How does a reverse mortgage work?

Reverse mortgages, also called Home Equity Conversion Mortgages (HECM), solve a large problem for seniors. They convert a portion of their home’s equity to cash – allowing the home owner to access their equity without creating a new monthly payment or forcing the sale of the home. That all sounds great – but how does a reverse mortgage work? And more importantly what are the risks of taking out a reverse mortgage?

Let’s cover the basics of a reverse mortgage. We’ll dive into how they work using a fictitious couple as an example and explore a few scenarios that may occur after the close of the loan.

If you haven’t had a chance to read up on what a reverse mortgage is or why it’s useful, you can read our article here. Otherwise, let’s jump into the nuts and bolts of how these loans work.

How does a HECM loan work?

The easiest way to explain how a reverse mortgage works is to walk you through one. Let’s start our example loan by introducing our borrowers – Bernie & Gertrude. For simplicity’s sake, we’ll round the numbers we use so they’re easy to follow, so don’t fret if you do the math yourself and they’re not exact!

Bernie is 71 years old, Gertrude is 67. They’ve been married for 45 years and have five adorable grandchildren who they love to spoil. They live just north of Santa Barbara, California, in a home worth $400,000.

Bernie is 71 years old, Gertrude is 67. They’ve been married for 45 years and have five adorable grandchildren who they love to spoil. They live just north of Santa Barbara, California, in a home worth $400,000.

When it comes to housing payments, they have a small mortgage on the house ($40,000) at an interest rate of 4%. Their monthly payment is $191. The property taxes on the home are $4,000 a year, or $333 per month. Homeowners insurance is $995 a year, or $83 per month. They do not pay an HOA fee for their home, so outside of their mortgage payment, their monthly costs are $416.

Bernie & Gertrude have an income of $3,000 per month – this is a mix of social security benefits & their retirement income. They had hoped to make $48,000 a year ($4,000 per month) but, like many retirees, they came up short on their savings. They’ve been making due by keeping their expenses low, but life threw them some curveballs.

Recently, Bernie’s hip was acting up, and he had to get it replaced. By the time he paid for his insurance deductible, physical therapy, medication, and everything else, Bernie’s bill totaled $15,000.

Gertrude’s car also broke down shortly after, and the cost of getting her transmission fixed was $3,000. To make matters worse, their air conditioner unit went out and needed to be replaced – between buying the new unit & paying to have it installed, the bill was $5,000. It was a rough couple of months, with these unexpected bills adding to $23,000.

With costs mounting, and their monthly income already spread thin, Bernie decided to research reverse mortgages.

How much can you get with a reverse mortgage?

Bernie would like a $25,000 lump sum when he closes his loan (enough to cover his expenses plus a little cushion). He would also like to draw some money every month to supplement his income. So how much can he actually get?

Reverse mortgage lenders use a few factors to determine how much you can qualify for – this amount is called the principal limit. For reverse mortgages, this principal limit is similar to the LTV ratio for a conventional loan – it’s a measure of risk, and it exists to protect everyone’s interests and investment.

HECM principal limits

There are a few things that affect your principal limit. The first limit is defined by the FHA –

- FHA lending limit in the area – The maximum amount Bernie can take is based on FHA guidelines, which ranges from $314,827 to $726,525 in 2019. For most of the country that number is around $400,000, but there are exceptions for high-cost living areas. You can learn more about your local limit here.

- Home’s appraised value – the lender takes the lesser of the lending limit and your home’s appraised value. You can learn more about the home appraisal process and how it affects your mortgage here.

Back to our eample, Santa Barbara County is considered a high-cost area, so let’s say the lending limit is $726,525. However, Bernie’s home is valued at $400,000, so his appraisal value will be used to calculate his principal limit.

Initial interest rate vs expected interest rate for reverse mortgages

The next factor that affects your principal limit is your reverse mortgage interest rate. There are two interest rates that come into play here, and they serve different purposes –

Initial interest rate (IIR) – this is the actual interest rate for your loan. It’s the interest amount you pay for money you borrower. Your lender will provide this to you when you apply for the loan.

For fixed rate loans, the initial interest rate will never change. Borrowers who are taking a lump sum from their HECM loan can qualify for a fixed interest rate.

Borrowers who want monthly payments from their lender only qualify for adjustable interest rates. For adjustable rate mortgages (ARM loans) the rate can fluctuate over time, and is usually tied to an index value. In most cases, the maximum interest rate for a reverse mortgage is capped at a certain amount.

Expected interest rate (EIR) – This interest rate does not affect the interest rate of your loan, or how much you are required to repay. Instead, this is the rate that the lender uses to determine your principal limit. This number is usually higher than your internal interest rate, and it accounts for things like your closing costs, mortgage insurance, and other costs. It’s similar to the difference between your interest rate and APR on a conventional mortgage.

By accounting for the total cost of the mortgage up front, the expected interest rate makes sure the lender does not provide too much money to the borrower. This protects the home, ensuring it doesn’t go underwater, which would be bad for both the borrower and the lender.

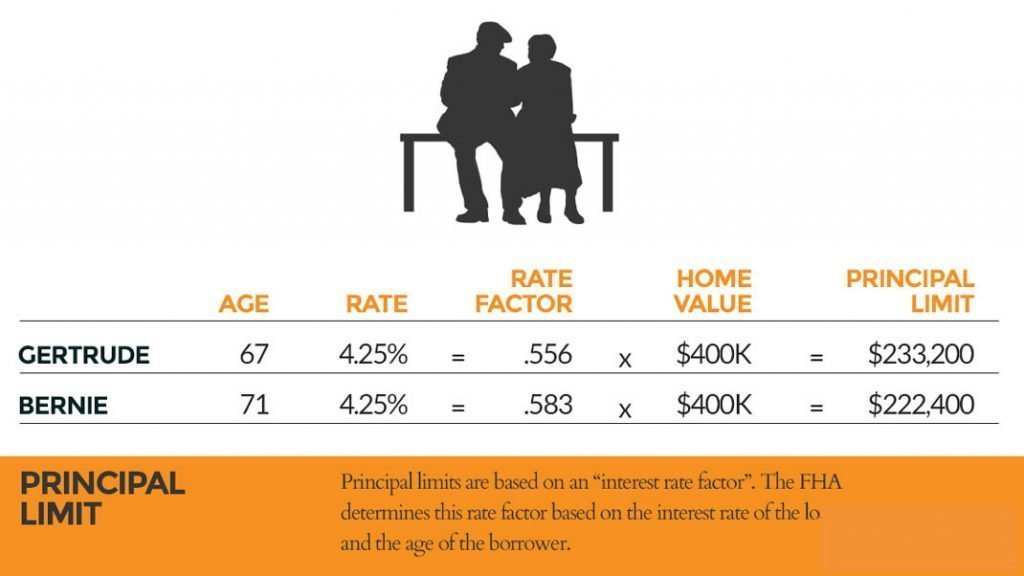

The expected interest rate comes from the FHA, and it’s based on a few factors, including age of the youngest borrower and your initial interest rate.

Because Bernie wants both a lump sum and monthly payments, he must get an adjustable rate mortgage. When Bernie got a quote his rate was based on the 1-month LIBOR rate, which was .435% at the time. The lender margin was 2.5%, and the mortgage insurance on the loan was 1.25%. Add those all together and Bernie’s initial interest rate would be 4.185%.

Based on this rate, and their expected interest rate, we can calculate the principal limits for Gert & Bernie:

The principal limit is based on the youngest borrower. We use Gertrude’s principal limit, which means as a couple they can borrower up to 55.6% of their home value, or $222,400.

If this sounds hard don’t worry – your lender will do this calculation for you. You can also visit this FHA page to download the latest table and estimate your rate, which will allow you to calculate your principal limit yourself.

Converting home equity into a reverse mortgage

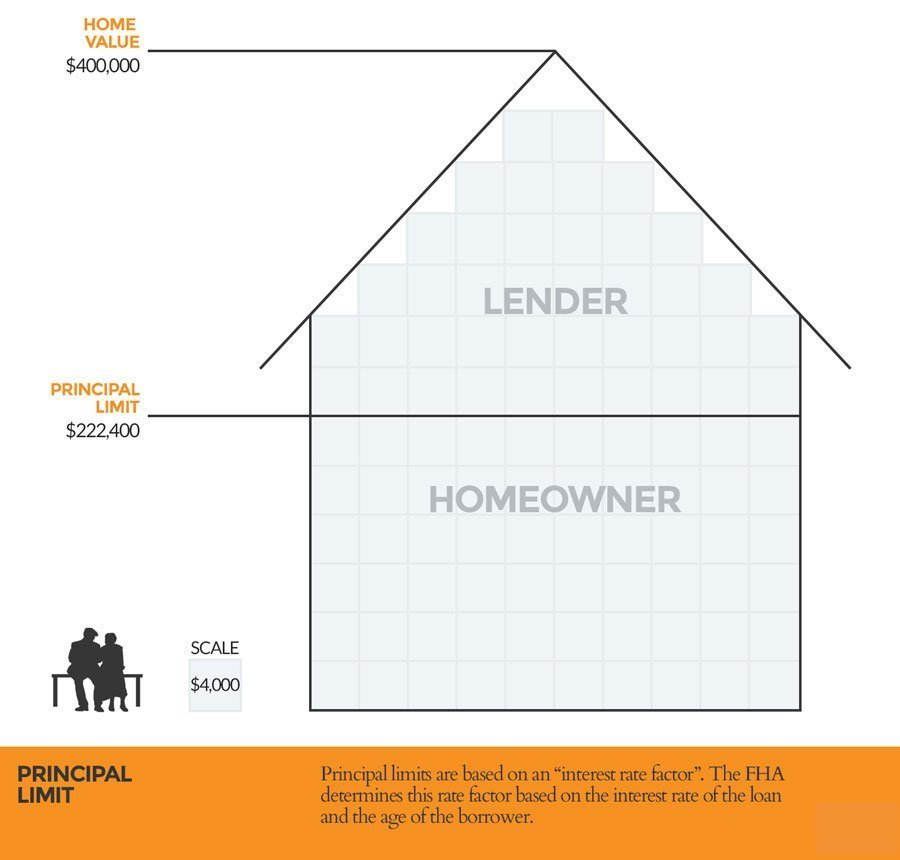

Imagine your house was built of legos. If your house was worth $400,000, and was made of 400 lego bricks, each brick would be worth $1,000.

Your principal limit splits the home equity, allocating one part for the lender and one part for the homeowner. Some of the bricks are set aside for you, and you can exchange them for cash. This is your principal limit.

The rest of the bricks are set aside for the lender. As you pull cash out of the home, either in a lump sum or with monthly draws, the lender takes some of those equity bricks as interest.

Once you divide the home equity it would look like this:

The lender doesn’t get to keep all the equity bricks in their group – only the ones that get used for interest. And they can’t do anything with their equity either. They have to wait until the borrowers pass away or the house sells before they can “cash in.”

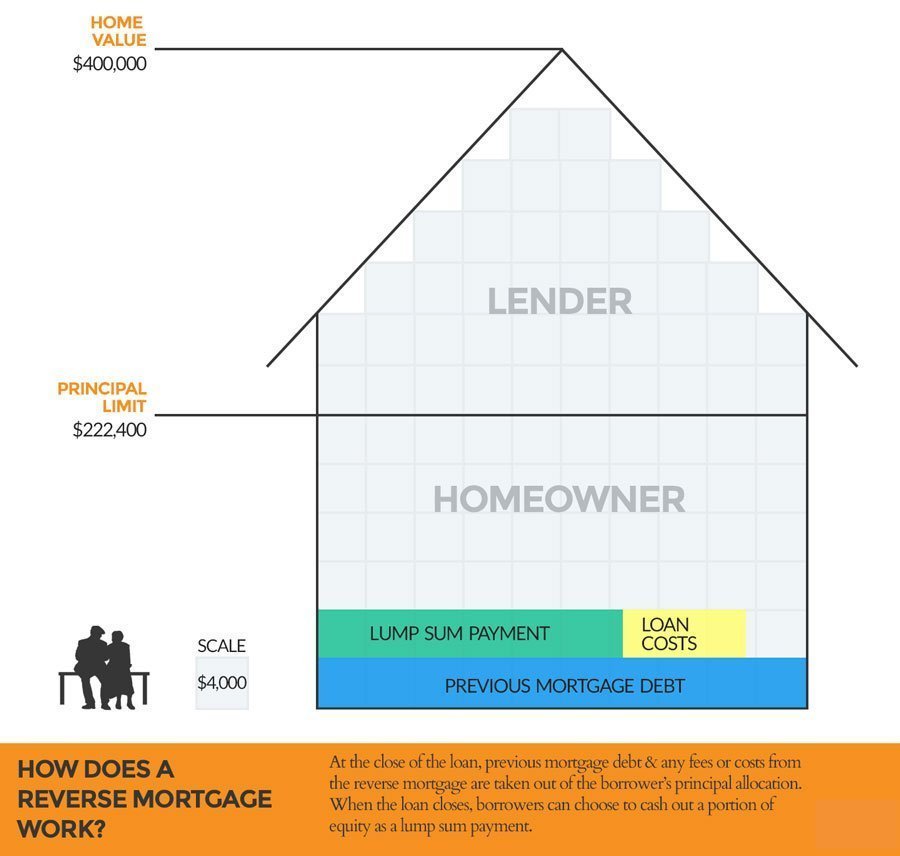

From here, we need to start deducting costs & expenses. These come out of the homeowner side of the equation. Starting with the principal limit, we’ll subtract –

- Loan Costs – the lender will take their costs out of the principal amount of the loan. For Bernie’s quote, these costs were $10,555 between the lender fee, upfront mortgage insurance premium, and various other costs like appraisal and title.

- Current mortgage amount – the lender will also pay off the existing mortgage of $40,000.

This brings Bernie’s available principal from $222,400 to $171,845. From there, Bernie will take out his $25,000 in cash as a lump sum to cover his bills. The image below shows how all of these costs would affect the home equity.

This leaves $146,845 available for the homeowners. Based on their expected interest rate, that means our couple could receive $790 per month to supplement their income. Every month, $790 will be removed from Bernie & Gertrude’s principal, and the interest accrued on that money is accounted for in the lender’s allocation.

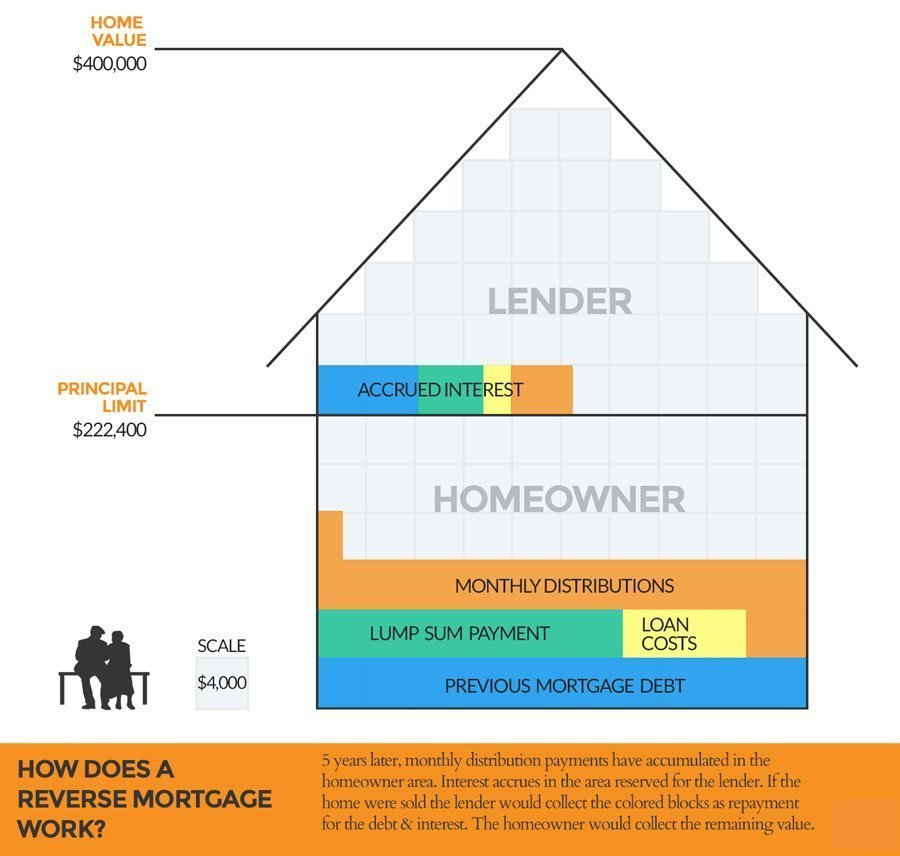

This costs for the loan, the cash taken as a lump sum, and the cash used to pay off the previous mortgage debt will also accrue interest every month. This will be accounted for in the lender’s side of the equation.

To illustrate these monthly distributions & the effects of interest, let’s see what the home equity would look like after 5 years:

Is a reverse mortgage a good idea?

That depends on your situation. But in this case it could have been a positive thing for our sample couple. Because they paid off their old mortgage, they eliminated a $191 monthly payment. At the close of their loan, Bernie & Gertrude covered all of their bills, created a small emergency fund for themselves, and freed up an additional $981 every month – by eliminating their previous mortgage payment and raising their monthly income from $3,000 to $3,790.

Reverse mortgage FAQs

Bernie & Gertrude solved their short-term financial issues – but how does this new loan affect them long term? Let’s walk through some common scenarios.

- What if the debt from the loan is more than the home is worth?

- How does a reverse mortgage work when you die?

- How long do heirs have to pay off a reverse mortgage?

- How long does a reverse mortgage last?

- How do you pay 0ff a reverse mortgage early?

- Can you sell a house with a reverse mortgage?

- What if my home value goes up?

- What if my home value goes down?

- What if interest rates go down?

- What if interest rates go up?

What if the debt from the loan is more than the home is worth?

What if the home depreciates so much that it goes underwater? Or our couple lives an incredibly long and fruitful life well into their 110’s? Will Bernie, Gert, or their adorable grandchildren be responsible for this debt?

HECMs are non-recourse loans, which means you will never owe more than the value of the home. The lender is not allowed to go after the estate or the assets of the heirs to satisfy any debt.

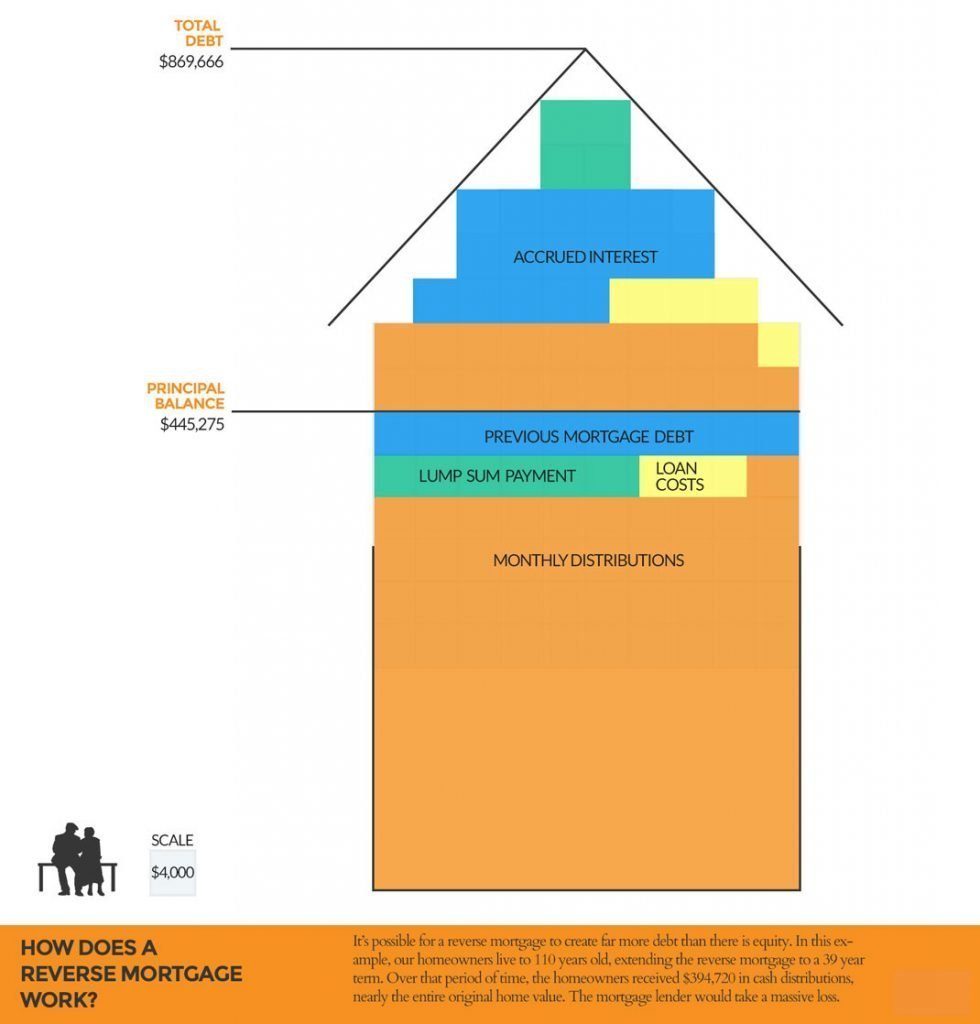

Let’s pick an extreme scenario and walk through it. First, let’s say Bernie & Gert live for another 39 years after getting their loan – this puts Bernie at 110 years old & Gertrude at 106. Let’s also assume that after 39 years the home has not changed in value, and that interest rates have not moved.

After 39 years, or 468 months, here’s how everything breaks down:

- Loan costs – $10,555 in principal, $17,227 in interest. Total cost of $27,782.

- Previous mortgage debt – $40,000 in principal, $105,286 in interest. Total cost of $145,286.

- Lump sum cash distribution – $25,000 in principal, $40,804 in interest. Total cost of $65,804.

- Monthly payment distributions – $369,720 in principal, $301,075 in interest. Total cost of $670,765.

At this point, the home equity would look like this:

In this (unlikely and ridiculous) scenario, the $400,000 home has $869,667 in debt (we had to blow the roof off the house to make all that debt fit!) When the home is sold, the 5% commission would tack on another $20,000. This is by far the worst possible scenario for the lender – when the home is sold, they will get $380,000 (sale price minus the commission) to pay off nearly $870k worth of debt. They will lose a staggering $490k on this loan.

The real question is how did our couple fare in this scenario? First, they ended with $0 in home equity when all is said and done. So what did they gain? Of the $869,667 in debt Bernie & Gertrude received $394,720 over the life of the loan – nearly the entire cash value of the home. This includes their $25,000 lump sum payment as well as 468 monthly payments of $790. They also eliminated any mortgage payment in the process, drastically reducing their housing costs.

Again, this is a nearly impossible scenario. The home value would have fluctuated over time. The interest rates would have moved up & down a number of times. While Gert & Bernie could have lived to 110, the chances of them living in the same home for the entire time are slim.

That being said, this scenario is an interesting test case – it illustrates the risks involved with a reverse mortgage for both the lender and the borrower.

Bonus – If you are like me, you are wondering what 39 years of modest appreciation would do to the home value. This doesn’t make our example any less ridiculous… but with a consistent 2.5% rate of appreciation, Gert & Bernie’s $400,000 home would have been worth $1,047,174 after 39 years.

How does a reverse mortgage work when you die?

What if Bernie & Gertrude were to perish in a tragic skim boarding accident 5 years after getting their loan? This would trigger the loan to become due, and their heirs would have to satisfy the debt. They’d have the same options available to them in the “payoff” scenario. If they wanted to keep the home, they could pay off the debt in cash, or get a “forward” mortgage to refinance it. The total debt after 5 years is $143,642, which would lead to a very reasonable 36% LTV loan.

If they were not interested in keeping the home, or they were not able, they could sell the home. In the case of a sale, they would pay the associated fees as well as the outstanding debt, and they would get to keep whatever equity was left. In our example, Gert & Bernie’s family would walk away with $236,359 after paying the outstanding debt, fees & commissions.

How long do heirs have to pay off a reverse mortgage?

HECMs are non-recourse loans, which means you will never owe more than the value of the home. Regardless of the total amount of the debt, the lender is not allowed to go after the estate or the assets of the heirs to satisfy any debt.

How long does a reverse mortgage last?

Bernie & Gertrude’s loan distributions were based on tenure – that means as long as one of them is living in the home as a primary residence, and they make their other payment obligations (like property tax, homeowners insurance, etc.) they will receive the monthly payments. This is regardless of how long they live for.

Even if the lender ends up paying more than the total cost of the home, as long Gert or Bernie meet the criteria, they’ll continue to get their payments.

The other options for taking out cash with a reverse loan are –

- One-time lump sum – borrower receives a single, lump sum payment. In this case, the borrower would be eligible for a fixed rate mortgage.

- Term – the borrower receives monthly payments for a fixed period of time.

- Line of credit – borrowers have access to a fixed amount of money. They can use this money as they need it, and can draw upon that money up to their principal limit amount.

- Modified tenure – a combination where borrowers receive a line of credit AND monthly payments as long as they occupy the home.

- Modified term – a combination where borrowers receive a line of credit AND monthly payments for a fixed period of time.

How do you pay off a reverse mortgage early?

Say our couple did not want this reverse mortgage any longer. What are their options?

With HECM loans, borrowers have a “right of recision.” This means that within 3 days of closing the loan, they can change their mind and call it off. The loan goes away, the lender will refund any money that was collected, and it was like it never happened.

What if that three day period has passed? What if they want to get rid of the loan 3 years later? At any time, if the borrower no longer wanted the loan, all they need to do is repay the outstanding loan balance. They can do this in a number of ways –

- Pay the debt off in cash

- Sell the home & use the proceeds to pay off the reverse mortgage

- Refinance the loan into a traditional “forward mortgage” – like a conventional loan you’d use to refinance a house normally.

Can you sell a house with a reverse mortgage?

What if Gert & Bernie find a nice retirement community, with a full-time nursing staff and a sweet shuffleboard set up, and decide they want to move? They can sell their house just like they normally would.

Let’s say they decide to move 5 years after getting their loan. For simplicity’s sake, let’s assume their house didn’t appreciate over this time, and it was still worth $400,000. Their house looks something like this –

When they sell their house, they’ll have to pay:

- Fees and commissions to the realtor – We’ll assume this is 5%, or $20,000.

- Outstanding Principal Balance – which comes out to $122,955 in this case. This includes:

- Loan costs – $10,555

- Previous mortgage debt – $40,000

- Lump sum cash distribution – $25,000

- Monthly payment distributions – $47,400

- Outstanding Interest – which comes out to $20,686 in this case. This includes:

- Loan costs interest – $2,209

- Previous mortgage debt interest – $8,370

- Lump sum cash distribution interest – $5,231

- Monthly payment distribution interest – $4,877

This comes to a total of $143,642 in debt. Just like a conventional “forward” mortgage, everything else is theirs to keep. In our example, Bernie & Gertrude sell their house for $400,000 and walk away with up to $256,358 in their pockets.

It’s important to note here that the monthly distributions coming from the loan will stop at this point. When the loan is eliminated, Bernie will no longer get his $790 check every month, so his income will drop accordingly.

What if my home value goes up?

What happens if the home appreciates? Again, the lender is only entitled to the interest that has been accrued. The homeowners, or their heirs, are entitled to whatever is left.

What if Gert & Bernie’s house appreciated 10% over that same 5 year period? They are still required to pay the same fees, and pay off the lender’s debt – but they’d pocket the extra $40,000 in appreciation. If they sold their home for $440,000, they would walk away with $276,359 at the close of the sale.

What if my home value goes down?

What happens if the value of the home goes down? Let’s say Bernie’s houses loses $20,000 in value (5%) over 5 years. It only sells for $380,000.

Like the other scenarios, the lender is only able to collect what interest was accrued. The homeowner or their heirs are entitled to whatever is left over.

In Bernie’s case, the total amount due to the lender is still less than the home value, so a sale is handled no differently. Our couple walks away with $216,359 after selling at the depreciated value.

What if interest rates go down?

Like other types of home loans, you can refinance a reverse mortgage. Doing this will lower your interest rate. Depending on how much rates have moved, this may increase your principal limit, which could allow you to increase your monthly distribution amount. If you are interested in getting a rate quote you can visit our partner Quicken Loans here.

What if interest rates go up?

An increase in rate could affect your reverse mortgage. As discussed in a previous article, borrowers who choose to receive monthly distribution payments will have loans with an adjustable interest rate. In our example, Bernie & Gert’s rate was tied to the LIBOR index.

If the index rate for a loan goes up, the interest rate for the loan will rise accordingly. This will not affect the monthly distribution amounts our couple receives – that monthly payment to the borrower will remain constant.

However, it will affect the amount of interest charged for the outstanding debt. This is part of the reason why lenders calculate the principal limit for the loan based on an expected interest rate – they want to account for a potential interest rate increase.

Most of these loans have a lifetime interest rate cap. This means that regardless of how much rates rise, the borrowers have a defined maximum interest rate. For Gert & Bernie the lifetime cap on their loan was 12.934%. To reach that cap, the LIBOR index would need to rise from .434% to 9.184%. Said another way, the index would need experience a 2100% increase – while not impossible, this seems highly unlikely that our couple will hit their interest rate cap.

Like any adjustable rate mortgage, you should do your research to understand the risks long before you sign up for the loan.

Learn more about reverse mortgages

Still have questions? Read more about the pros and cons of reverse mortgages here, or check out our helpful list of 17 facts you need to know about reverse mortgages.

{kind=link}