What credit score do I need to buy a house?

Mortgage companies take a lot of things into account when you apply for a home loan. A major factor in qualifying is your credit score. But what credit score is needed to buy a house?

This question actually breaks down into two parts:

- What is the minimum credit score to buy a house?

- How does your credit score affect your mortgage?

What is a credit score?

A credit score by definition is a three digit number calculated based off of information from your credit report and is one instrument used by lenders to determine your creditworthiness for loans or a credit card. In the U.S., there are three major credit bureaus that issue these credit reports. Your credit score(s) can qualify you for approval and it determines your interest rate.

Different lenders can each have a unique set of standards for what they consider to be a bad, poor, fair, good, or excellent credit score, so it is considerably important to continue building your score to receive the best interest rates and higher rates of approval.

When people talk about credit scores, what they are usually referring to is actually a FICO score. The Fair Isaac Corporation (FICO) was created in 1956. Two guys (with the last names Fair and Isaac) created a scoring system to judge a person’s creditworthiness. To this day the company provides this same service to lenders, although the scoring system has undergone a number of changes.

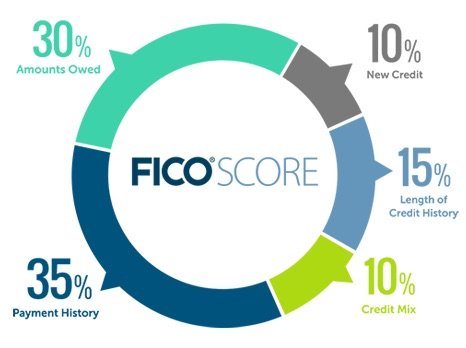

Your FICO score is calculated based on five criteria. In order of importance, they are

- Payment history – If you’ve paid your debts in the past, you’ll probably continue to pay them in the future.

- Amounts owed – If you are deep in debt, and your credit cards are maxed out, you’re a riskier customer to lend to.

- Length of credit history – With age comes experience. The longer you’ve used credit responsibly, the higher your score.

- Credit mix – What types of debt do you have? If you have 10 credit cards that may be a red flag. But 5 credit cards, a mortgage, 3 student loans & an auto loan gives you a balanced credit profile.

- New credit accounts – If 8 of your 10 credit accounts were opened last week, that’s usually a red flag. You might be in some financial trouble.

There are three different companies, called Credit Bureaus, that monitor your FICO score. The three bureaus are Equifax, Experian, and TransUnion. Each looks at different aspects of your credit history, so your score for each bureau is usually slightly different.

Mortgage credit scores are different than the rest

Many people don’t realize this, but these companies actually have different calculations based on what type of credit you are applying for. Your credit score for a student loan is different than your score for a credit card, which is different than your score when applying for a mortgage.

No one knows exactly how these scores are calculated, but we do know a fee things about how mortgage credit scores differ from normal –

- They tend to be lower

- They are generally more sensitive to missed payments

- They are generally more sensitive to the length of credit history

This all makes sense. Your mortgage will most likely be your largest debt. Mortgages also have very long terms, up to 40 years in some cases. It’s understandable that mortgage lenders value these aspects of your FICO score.

Minimum credit score to get a mortgage

There is no single minimum score – there are a few minimum scores based on the type of loan you want & which mortgage company you apply with.

- The minimum credit score for mortgage loans is 580, which is offered for FHA loans.

- For conventional loans with a fixed interest rate the minimum credit score is 620.

- For conventional adjustable rate mortgages, the minimum credit score is 640.

These are the minimum FICO scores required for government backed loans that fall under the qualified mortgage guideline.

On top of the government guidelines, some mortgage lenders have their own minimum scores. Even though you meet the requirements for the loan, if your score is low you might have to shop around for the right mortgage company.

If you have a score that is under these limits you still have options. For instance, you can still qualify for some FHA loans if your score is under 580, but you will need a down payment of at least 10% of the home price.

Let’s say you want to buy a $250,000 home. If your credit score is 580 or more, you can use a 3.5% down FHA loan. This means you only need $8,750 for a down payment ($250,000 x 3.5%).

If your score is below 580, you are required to put 10% down, which means you will need $25,000 in cash to buy the same home.

In cases like this, you may be better off working to increase your score or even paying a credit repair agency to help you. Once your score is above 580 you will be eligible for the 3.5% loan again – spending some time and a few hundred dollars now to fix your credit could reduce your down payment by $10,000+.

If you are interested in working with a credit agency, we like these companies –

- CreditRepair.com – Customers see an average increase of 40 points in 4 months, sometimes more.

- Lexington Law – They had over 7 million removals in 2014 alone. Because of their experience and their history, they know how to fix errors quickly.

How does your credit score affect your mortgage?

Ready to have your mind blown? Credit scores don’t matter nearly as much as people think. After a certain point, they hardly matter at all actually.

Your credit score affects two major aspects of getting a home loan: qualification and interest rate

Qualification – Is your credit score high enough to justify getting a loan? As we mentioned, many lenders have a minimum FICO requirement. While some lenders may dip into the high 500’s, a score above 600 is usually enough to get you in the door. Some specialty products have a higher minimum score. But for the most part, pass that minimum score test and you’re ready to move forward.

Interest rate – The lower your credit score is, the more risky your loan seems. This added risk means the lender increases your interest rate. Determining your interest rate with respect to your credit score is called “loan pricing.”

Credit scores are usually grouped into tiers during pricing. Tiers can vary widely, but for every 20-50 points difference in your score (depending on the lender) you move up or down a tier. Each tier usually equates to a interest rate adjustment of .125 – .25%. Most lenders have a top tier where, above a certain credit score, it’s all the same. In many cases that top tier score is around 780.

To give you an idea of how your credit score will affect your interest rate, we put together the table below. The table shows how much the cost of your loan will increase based on your credit score and the loan-to-value ratio (LTV) of your home.

This example is for Fannie Mae loans. We used some common LTV amounts, but you can view their entire pricing adjustment matrix here.

How credit score impacts interest rates

You can see how the mortgage interest rate you qualify for changes based on your credit score by changing the credit score in the calculator below.

Again, the adjustments that are made based on your credit score will differ. It depends on which loan product you use and which lender you apply with. But there are a few common “rules” –

Credit scores as broken down into 20 point tiers – If you fall into one of these tiers your pricing will often be the same. There is usually no difference between a 641 credit score and a 650 score as far as interest rates go.

The top tier is 760+ – If your score is above 740 points you will usually get the best pricing. When applying for a loan, someone with a score of 770 will generally get the same interest rate as someone whose score is 810.

There are benefits to having a higher score – Borrowers with high credit scores have more negotiating power. If you have a score of 760+ you can often negotiate discounts – getting the lender to discount fees or even lower the interest rate. The thing is you have to ask for these discounts, they won’t just give them to you!

Increase your score prior to applying for a mortgage

If your credit score is low (or just lower than you’d like) then this article is for you. It’s no secret that having a higher credit score means a better chance of getting approved for a loan. There is a minimum score you need to qualify for certain things (like a home loan). But it’s important to know that your credit scores affects a lot of other aspects of your life.

Of course, it’s the biggest factor when a company is deciding whether or not you deserve credit. But it also determines what interest rates you’ll pay, it can affect your insurance rates, it can even affect your ability to get a job.

You can use any (or all!) of these methods to try to raise your score before applying for a mortgage, student loan, or any other credit application.

Understand where you’re starting from

The Karate Kid didn’t defeat Cobra Kai overnight – he had to start by detailing Miyagi’s car. Before you do anything, you need to know your credit score, that way you can track your progress.

The most important scores to know are your FICO scores from each of the 3 credit bureaus (Equifax, Transunion, and Experian). These scores are used in a whopping 90% of all credit decisions in the United States. It’s important to note that services like CreditKarma aren’t providing your FICO score, but rather an approximation of your score that isn’t always accurate.

The only way to view all of your FICO scores is to go to myfico.com. Not only will you get a 3-bureau credit report, they will give you the 28 FICO scores most widely used in mortgage, auto, and credit card lending.

It’s the best way to accurately assess where your score is, check for errors, and ensure the information being reported is accurate. We’ll cover this in a bit, but 1 in 5 people have errors on their credit scores – if you don’t use a tool like myFICO, or pay for the reports direct from the bureaus, you may not catch an issue that is unfairly dragging your score down.

Because myFICO goes direct to the bureaus, you have to pay for it – we recommend doing this once if you haven’t gotten a detail report direct from the bureaus.

Tips to improve your credit score

Fix Major Errors In Your Credit Score

If you come across errors or mistakes on your report, these are the easy ways to quickly improve your score and you can often fix them yourself. All three of the credit bureaus allow you to dispute items online. You can dispute errors here:

Here are a couple of tips to consider when disputing information on your credit reports.

- A creditor has 30 days to respond to a dispute before the dispute result is automatically granted in favor of the consumer.

- Negative items – such as an account sent to collections, a charge-off, or a bankruptcy – are only permitted to stay on your credit reports for 7 years.

- In some cases negative items may not fall off automatically, so it’s good to periodically check to make sure they are removed in a timely manner.

Pro tip: To make sure negative items were removed from your credit profile, it is best to get your credit report direct from the bureaus. This is a case where paying for a report from a company like myFICO is worthwhile – you will get reports directly from all three bureaus, which is the best way to make sure your errors were handled properly.

Sometimes there are major errors – if you have had a divorce, major medical expenses, delinquencies, bankruptcy, foreclosure, or any other major event that could impact your credit, you might want to enlist the help of a professional.

Lexington Law helped remove 7 million+ errors in 2014 – they have a ton of experience and success in removing negative marks, and their experience means they work quickly. Simply put, they’re the largest and most efficient credit repair company out there.

If you have major issues and you don’t want a full blown law firm, you can also check out CreditRepair.com – they’re online, work quickly, and they see an average jump of 40 points in 4 months.

Open a secured credit card

For FICO to even track your credit score, you need a minimum of one account that has been open for at least 6 months. That account must be reported to one of the credit bureaus, and you cannot be dead. If you’re reading this, you’re alive, which means you’re 1/3 of the way there.

A secured card is a great way to kick off your credit journey and make sure your score is reported. Basically it works like this:

- Deposit money into a special savings account. The bank that issues you a card will use that money to collect any missed payments.

- Whatever amount you deposit becomes your credit limit. This eliminates the bank’s risk, so just about anyone with some extra cash can get their hands on a secured credit card.

- After 6-12 months of usage and on-time payment, you can ask your creditor to be upgraded to a normal (unsecured) credit card.

- When your request is granted, your creditor will give you your deposit from your secured card back.

Secured cards are great because it’s impossible to spend more than your limit. Technically you’re not even going into debt since the bank has your deposit. It is simply a tool to help establish credit.

The best banks to get secured credit cards from are local credit unions. This is because bigger banks, such as Chase and American Express, either never offered or no longer offer secured credit cards.

Pro Tip: When applying for a secured credit card through a local credit union, make sure to verify that they will report your payment history to all three of the credit bureaus.

No More Late Payments

Payment history is the biggest factor in calculating your credit score. The easiest way to make sure that a payment is never late or missed is to automatically have them deducted from your checking account. Auto payments are ideal, but at the very least you should set payment reminders for yourself.

If something happens and you forget to make a payment – for whatever reason – contact the creditor immediately and directly ask if they would remove the late payment and any fees. Many will do this as a one-time courtesy – but keep in mind that asking nicely may only work once or twice.

Negotiate with your creditors

If you’re having trouble making payments, call the creditor directly. More often than not, they are willing to work with you to make sure that they get all – or at least some – of their money back.

Pro Tip: It never hurts to call and ask a creditor to lower your interest rates.

It’s not easy, but if you do your homework and are motivated, you can negotiate quite a few things. You can work with your creditors to establish a payment plan that you can actually afford. You can also ask them to lower your interest rate, reduce your total debt amount, or both.

Settle Collection Accounts

When you get your credit report, you may have some debts that have gone to collections. Sometimes you can quickly raise your score by dealing with these issues on your report.

Collection accounts affect your credit for 7 years. First, you need to decide if you want to address the issue at all. For example, if the collection account is 5 and 1/2 years old, you might be better off just waiting until it goes away.

If the issue is recent, or you can’t wait, then you have a few options to remove collections from your credit report. This can be tricky though – if you acknowledge the debt, or do not get the proper documentation to prove the debt was settled, you can run into some trouble.

If you have large collection accounts ($1,000+) someone like Lexington Law or CreditRepair.com can be a huge help – they will make sure to document the process, and if they can help settle your debt for less than you owe, they end up paying for themselves!

Pay down your debts to reduce your credit utilization

If you’re anything like me, credit card debt gives you an overwhelming amount of anxiety. Paying down your debt will not only will you sleep better at night, but your score may also drastically improve. Your credit utilization rate is the second most important factor in calculating your credit score.

You calculate your credit utilization by adding up all of your debt, and dividing it by your total credit limit.

A decent utilization rate is 30% or less. Anything below 10% is great because it shows lenders two things:

- You use credit cards responsibly.

- You don’t rely on credit cards to pay your bills.

If you want an even higher score, aim to get your utilization down to about 5%.

Pro Tip: While having no credit card activity sounds good, a 0% utilization rate actually hurts you. If you don’t use your credit cards at all ($0 balance across the board), this doesn’t show lenders you know how to responsibly use credit cards – it just looks like you don’t use them at all (yes, it’s a total Catch-22!)

Don’t Close Old Accounts

When you close a credit card it can actually have some negative effects. Depending on your current balances, your credit utilization rate may take a significant hit, which can lower your score.

It is also important to keep your oldest cards open for as long as possible to help your average age of accounts. Closed accounts only stay on your credit report for 10 years before falling off.

Closing your oldest account also means that you now have one less account contributing to your positive payment history each month.

Pro Tip: If you want to close a credit card to avoid paying an annual fee, call the credit card company. Ask about a retention offer or request to be downgraded to a no-annual-fee card product. In most cases, your card issuer will do whatever they can to keep you as a customer.

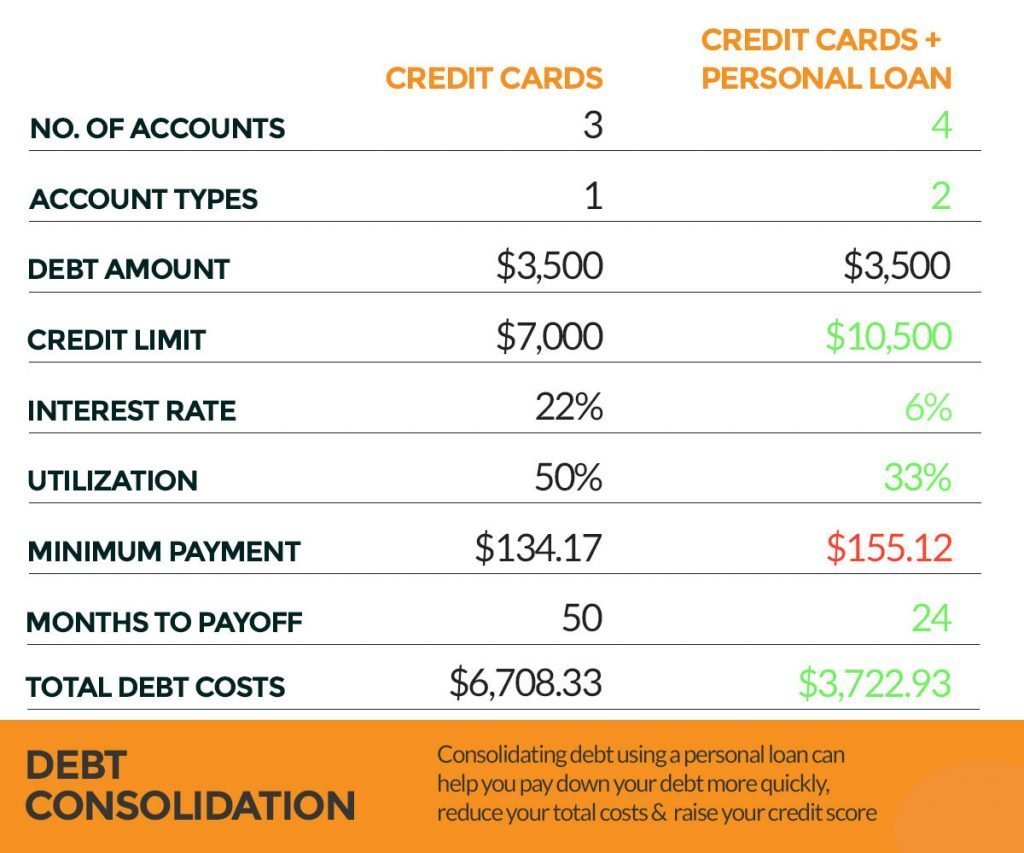

Consolidate and refinance debts

Another option that may make sense is to consolidate your credit card debt. Credit cards carry high-interest rates, anywhere from 15%+. Some even dip into the 30% territory, which is insane and predatory.

If you consolidate your debt, you can get a lower interest rate, which helps you pay down your loan faster. This also helps your credit mix (by adding a new account type) and can help your utilization rate (by shifting the debt & increasing available credit). Check it out below:

It’s easy to see that consolidating your debt could help your credit score, as a bonus it’s also a smart financial decision!

For debt consolidation, we recommend PersonalLoans.com. They use your information to give you multiple types of loan quotes – from Peer to Peer loans to Personal loans & even Bank loans.

With all these different consolidation options, it’s easy to quickly see if you can get a better interest rate and pay off your debt more quickly. It doesn’t cost you anything to get a quote, and if you qualify, you will get multiple offers almost immediately. If you have debt with an interest rate over 8%, it’s worth checking out PersonalLoans.com just to see what your options are.

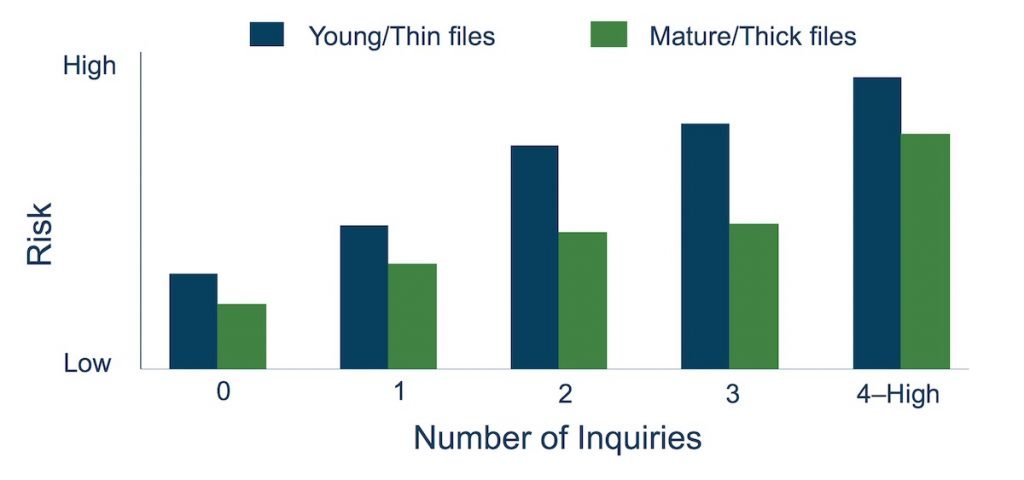

Minimize Impact of Credit Inquiries

Too many credit inquiries looks suspicious. Lenders think that you may be experiencing a financial hardship and are looking to max out your lines of credit.

It’s also important to note that credit inquiries have a much larger impact on young or “thin” credit files. The chart below, provided by FICO, shows how 3 inquiries on a “mature” credit profile has about the same impact as 1 inquiry on a thin file.

Courtesy of myFICO.com

A general rule of thumb is to hold off on any requests for credit starting 9-12 months before a mortgage application. For some, that may be difficult. If you are going to open new accounts, the least you can do is plan out your credit activity & then work to consolidate the inquiries.

Shopping for quotes from multiple lenders within a short and focused period of time can minimize the impact on your credit score. FICO’s scoring models view multiple inquiries for a single loan as only 1 inquiry. They will usually consolidate inquiries that are within 1-4 weeks of each other, but the closer together in time the better. While the inquiries will still appear on your credit report, only 1 will count towards your score; note that this does not apply to credit card applications!

Pro tip: Inquiries stay on your credit report for 2 years, but FICO only includes inquiries in the last year when calculating your score.

Learn which bureaus are impacted before applying for a new account

Use tools such as the Credit Pulls Database to view data-points from other applicants. This also shows you which lenders pull which bureau in each state. It will also help estimate your approval odds for a product from a specific lender. Hang on to this, it will come in handy in a second…

Put a Freeze On Bureaus

A security freeze, commonly used by victims of identity fraud, puts a hold on your credit and prevents opening a new account in your name.

Typically, you would navigate to each bureau’s website and pay a $10 fee to freeze your credit report, which blocks any activity until you contact them to unfreeze it.

A good way to raise your score is to freeze your credit report with the bureau that has your lowest credit score. This forces a creditor to pull your report from another bureau with a higher score, or a bureau with less inquiries. Controlling which bureau gets the inquiry lets you choose which score you present to the lender, and allows you to manage the impact of credit inquiries.

With a little work you can buy a house

For some people, owning a home is a key part of the american dream. And with a little bit of work to improve your personal finances it’s very attainable! To learn more about buying a home we recommend you check out our calculator for how much house you can afford. We also recommend learning more about mortgage interest rates and the difference between a pre-qualification and pre-approval early on in your home buying journey. As always, if you have any questions don’t hesitate to contact us!

{kind=link}