How to put an offer on a house

Maybe you fell in love with the first home you saw. Maybe it took you months, but your patience was rewarded with a beautiful house that hit all the sweet spots. However long it took, you’ve now reached the moment of truth – you’re ready to make an offer on a house.

You knew this time would come, but what does “make an offer on a house” really mean?

How do I determine the offer price?

The first step in crafting your offer is setting your offer price. How much are you willing to pay for the house? How do you even figure that out? This process is part art, part science.

Your realtor will find other properties that recently sold, a process called “pulling comps”. They’ll look for houses that are a similar size, have a similar number of bedrooms and bathrooms, in the same neighborhood, and in generally the same condition as the property you’re making an offer on. Realtor.com has an awesome search feature that can help you pull your own comps – it allows you to search an area for recently sold homes.

Based on those comparable prices, your realtor will start to make adjustments to account for things like recent moves in the market, other listings in the area, or differences between the comps and your target home. For example, if a comp has a pool, and the home you’re bidding on doesn’t, the realtor will adjust the comparable price down to account for that. This is where the “art” part of crafting an offer comes in.

Once they’ve gone through this process, your realtor will present this information to you. They’ll lay out the comps, explained why they chose those properties, and walk you through the adjustments they made. From there, you’ll work together to settle on an offer price.

How do I make an offer on a home?

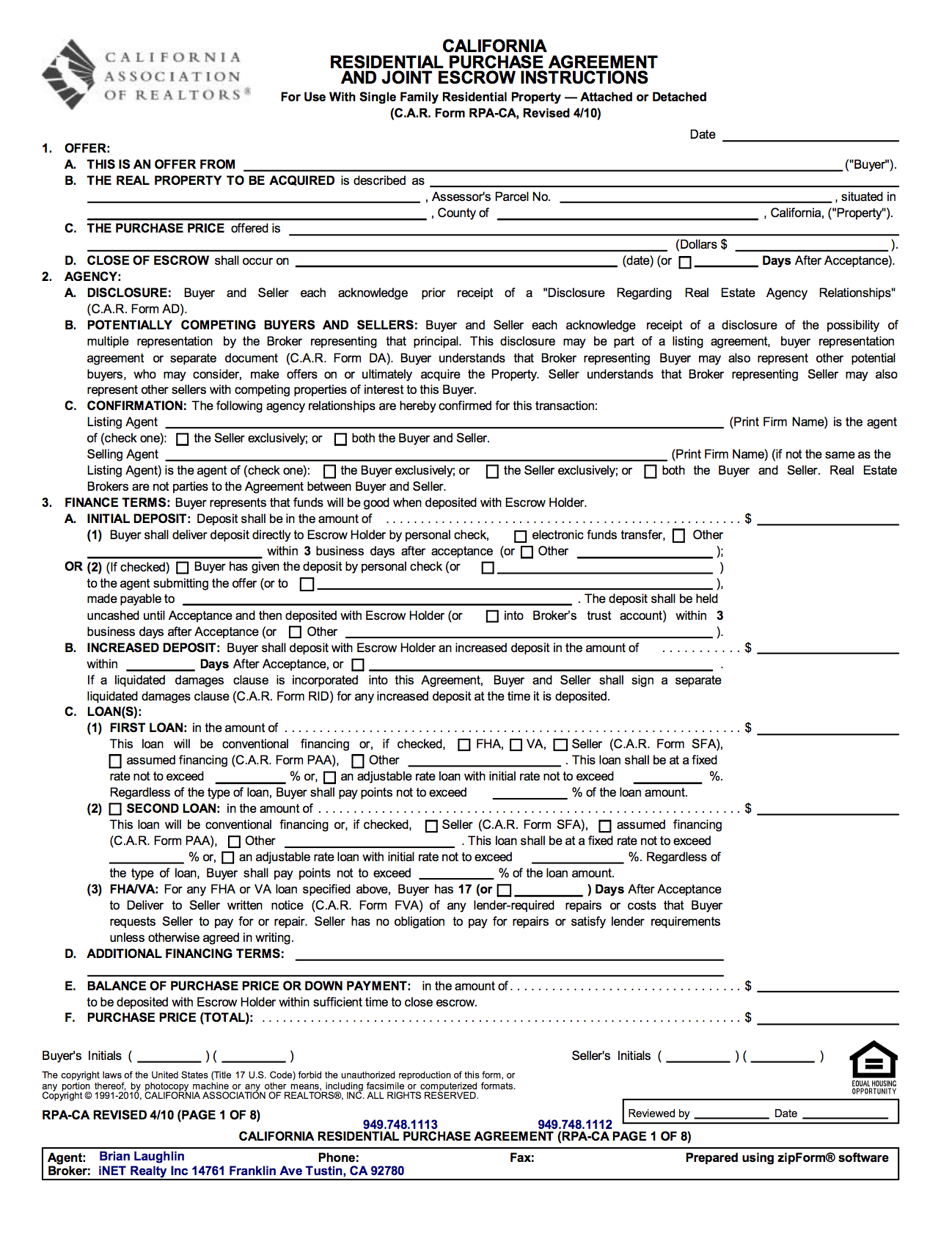

We’ll start with the mechanics. The actual offer itself is a piece of paper. Your real estate agent will have a standard agreement to use and will help you fill it out. The agreements vary state to state, but you can check out a sample offer here (officially called the “California Residential Purchase Agreement And Joint Escrow Instructions.)

Click the image to view the full agreement

Just because the agreement is standard that doesn’t mean you shouldn’t read it! There are a lot of little details that you’ll want to at least be aware of.

Purchase offers for a home usually spell out a few things –

The Basics – Your name, the address of the property & the price you’re willing to pay (the offer price.) These are the easy questions, bask in the fact that you know how to fill this out.

Real Estate Agents – You call out who your agent is and who the seller’s agent is. Another softball, you’re doing great.

Escrow terms – Now come the harder ones. The actual exchanging of money for the property can be sticky. To avoid issues, the exchange is handled by a neutral third party – usually a title company, escrow agent or an attorney. In the offer you’ll set a date for the transaction to take place, this date is called the “close of escrow.” Everyone has to have their respective parts complete by this part so the transaction can close. Since you are getting a mortgage, you’ll want at least 30 days before closing escrow, and your real estate agent or loan officer may recommend a longer period (45-120 days) depending on your situation or the seller’s preference.

Earnest money – When you submit an offer on a house you actually have to put some money on the line. A lot of first time home buyers are surprised by this. This money, called an earnest money deposit, proves to the seller that you’re a serious buyer. On average, you’ll need 1-2% of the home price as earnest money. That money will either be given to the escrow company or your realtor, who will in turn give it to the escrow company. If the deal falls through your earnest money may or may not be refunded to you – it depends on why the deal failed & how your agreement is instructed. Before submitting an offer make sure to ask your realtor about this!

Financial terms – this is where it helps to not only be pre-qualified or pre-approved for a loan, but to have a loan officer that knows your particular situation. You’ll have to spell out what type of financing you will use to purchase the home. You may also have to provide bank statements to prove you have the cash for your down payment & closing costs.

Who pays for what: Inspections and fees – There are a number of inspections, reports, fees & taxes that will be required to complete the purchase. You can negotiate who pays for these things, it is defined in the offer. Your realtor can advise you on how to handle this – in a hot market you may end up paying for these items to make your bid more attractive. In a buyers market, or with a home that is more likely to have issues come up during inspection, you can get away with asking the seller to cover these costs.

Occupancy – Here’s another curveball for you – you may not be able to move into your new house immediately after you buy it. Sometimes the seller will need time to find a new home, so in those cases you may jointly agree to rent the house back to them for a period of time. Being flexible with your move in date can be a big advantage.

Included items – There are a number of things (think appliances, washing machine/dryer, light fixtures, etc.) that may or may not be included with the purchase. What’s included and excluded in the deal is spelled out with your offer.

Title & Vesting – This part is really important. It lays out what everyone is required to do according to the contract. If any of these things don’t happen, the deal can fall apart. If it’s your fault as a buyer, you may lose your earnest money deposit. Make sure to cover this section with your realtor. Also go over the sections that cover remedies for breach of contract & dispute resolution. It’s always good to at least understand what happens if things go south, even if they probably won’t.

Legal stuff – These agreements have a ton of legal language. Disclosures are included so that everyone knows their rights, and to ensure that the buyer understands all the potential risks of buying the property. The house may have lead paint, natural hazards, etc. In a place like California, it could also be at risk for earthquakes, flooding, brush fires, natural gas explosions, or any other natural disaster (California really is a magical place.) The seller can be in trouble if they don’t alert you of these risks, so they’re included in the offer.

Once your offer is squared away, you’ll put that together with your earnest money deposit, your pre-qualification or pre-approval letter, and any other supporting materials (like your bank statements.) Your realtor will take this to the seller’s agent, who will submit the offer to the sellers. And then you wait (anxiously) to hear back.

Home offer and counteroffer process

The seller’s agent is legally required to present your offer to the seller within a few days. Still, waiting for a response can make the most hardened home buyer hyperventilate. I know for me, I swing wildly between “If they don’t accept my offer I’m just going to rent forever because no other house will ever compare” and “The house was an ugly color anyway, and it was small, and it smelled funny, they can keep it…” It’s a fine line between being excited and over committing yourself.

Eventually though, you’ll get a call from your agent. They talked to the seller’s agent and they want to meet to discuss. So you find a time to meet with them. And after all that build up – your agent has a counteroffer. Unless your offer is perfect, with everything the seller wanted and then some, they’ll probably have some revisions.

The only advice I can give here is don’t screw around too much. A lot of small back and forth negotiating can be draining for everyone. Pick your battles when responding to the counteroffer. Be upfront with your expectations, lay out what you’re willing to negotiate on, and be firm with your non-negotiable items.

If you go through this entire process and the sellers ultimately decline your offer, try not to get too discouraged. According to the National Association of Realtors, in 2014 the average buyer spent 10 weeks looking for a home, which doesn’t include the time the property spent in escrow. Buying a home can take months – it’s a marathon, not a sprint.

Bidding in a hot market

In some metro areas (Los Angeles, NY, San Francisco, Austin, Denver, and many more) the markets are hot. During the spring home buying season, they can get really hot. Like 20 offers on every listing hot – it’s a feeding frenzy. Buying a home in these areas can feel like an endurance challenge. However, there are a few things you can do to make your offer stand out.

- Be ready to make an offer quickly – if you hesitate in a hot market, someone is going to buy that home you fell in love with. Have your proverbial ducks in a row & be ready to make a move quickly.

- Get pre-qualified / pre-approved – Consider two identical offers: one with a lender’s stamp of approval for a certain purchase amount, another where the buyer hasn’t even spoken to a loan officer. Which offer seems more likely to close on time?

- Submit a strong offer – Don’t over extend yourself here, but if it’s within your range, consider submitting an offer at the list price, or potentially even higher than the list price. Is lowballing the seller to save $10 a month on your payment worth losing the house over?

- Understand the seller’s needs – Does the seller need to rent the property back after the sale? Or do they need to close within two weeks? Learn about their expectations as far as price, timeline, and negotiable items like fees & fixtures. Being accommodating can be a huge advantage.

- Make it personal – Buyers often underestimate the power of a personal connection. Some sellers have a deep, emotional connection to their homes. They may care about what’s going to happen to it when they leave or how their neighbors will be affected. Write a letter to go with your offer. Explain who you are, why you love the property, what your plans are for it, and why you love the neighborhood. A personal touch like this may help you win out over a stronger bid by someone a real estate flipper.

In some cases, you may find yourself in the dreaded “bidding war” with another buyer. The only advice I’d give you here is don’t get overly caught up in it. Anyone who has bought something on eBay knows how easy it is to get caught up in the excitement. You want to “win” the house. But if you end up offering more than you can afford, all you’re doing here is throwing away your earnest money and wasting time, which is hardly a win at all.

Why Realtors Matter

In my opinion, the offer process is where a realtor earns their keep. Their advice during this phase can be the difference between moving into your dream home or losing the house to another offer. It’s one of the many things that a realtor does to make your buying process easier.

They’ll have a good idea of what the house is worth. They’ll know how motivated the seller is. They’ll know how aggressive to be in negotiations. They’ll make sure the seller isn’t taking advantage by forcing you, as a buyer, to pay for unnecessary fees. A great realtor will brake check you before you get too caught up in a bidding war. And for those of you that avoid conflict like the plague, your realtor will handle the actual negotiating process, going back and for between you and the sellers agent.

A mistake in crafting the offer can easily lose you your earnest money. Not doing a key inspection, or not adjusting your offer based on the outcome of some inspections, can be a costly mistake as well. There is a tangible, financial benefit to working with a professional in many cases.

An offer accepted

Oh joy of joys! The seller accepted your offer. It’s awesome, scary, and incredibly exciting! Now it’s off to the races – you have until your close of escrow date to get that home loan!

{kind=link}