What is a reverse mortgage?

A reverse mortgage, also called a home equity conversion mortgage (HECM), is a tool that helps retired seniors borrower money against the value of their home. Reverse mortgages are designed to secure a comfortable living situation for retirees, help cover major expenses (like health care costs) and potentially generate monthly cash for the borrower.

Retiring is hard work

People aren’t great at seeing into the future. It’s actually a skill – its called affective forecasting. For whatever reason, we have a hard time considering our future self.

Daniel Gilbert studies this for a living. When it comes to estimating how much we’ll change in the future, or how happy something would make us, we are usually way off. He set up a really basic experiment with Prudential that shows how this inability to see into the future can affect retirement.

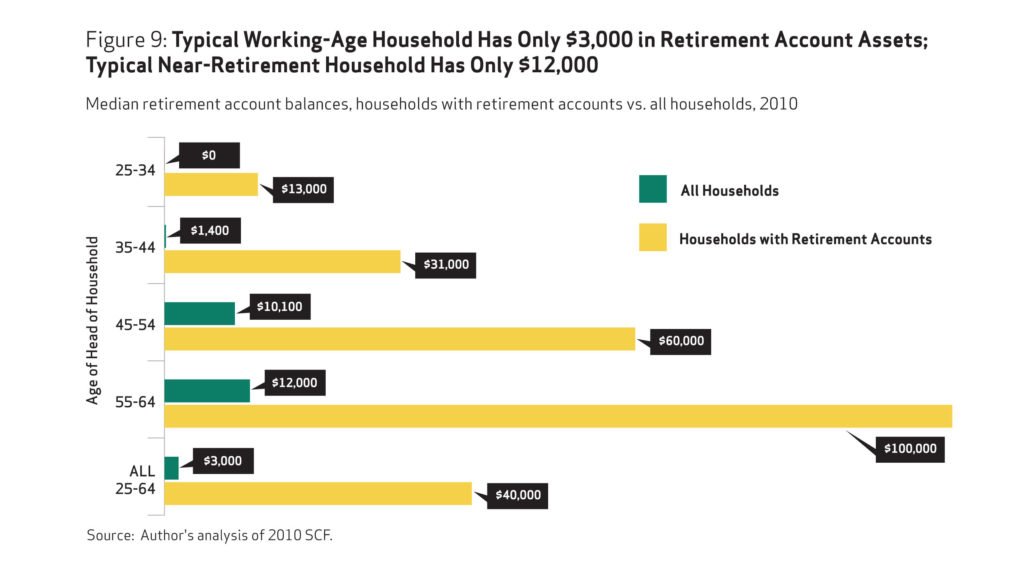

According to a 2014 report by the Employee Benefit Research Institute, nearly 42% of Baby Boomer & Gen X retirees don’t have the means for a 35 year retirement . When you break it down based on age it’s even scarier, older americans close to retirement haven’t saved nearly enough.

That’s a scary thought – these two generations have a combined 131 million people. That’s 56 million people who may not have enough money for retirement. A recent CNBC report stated that 40% of baby boomers have no retirement savings at all.

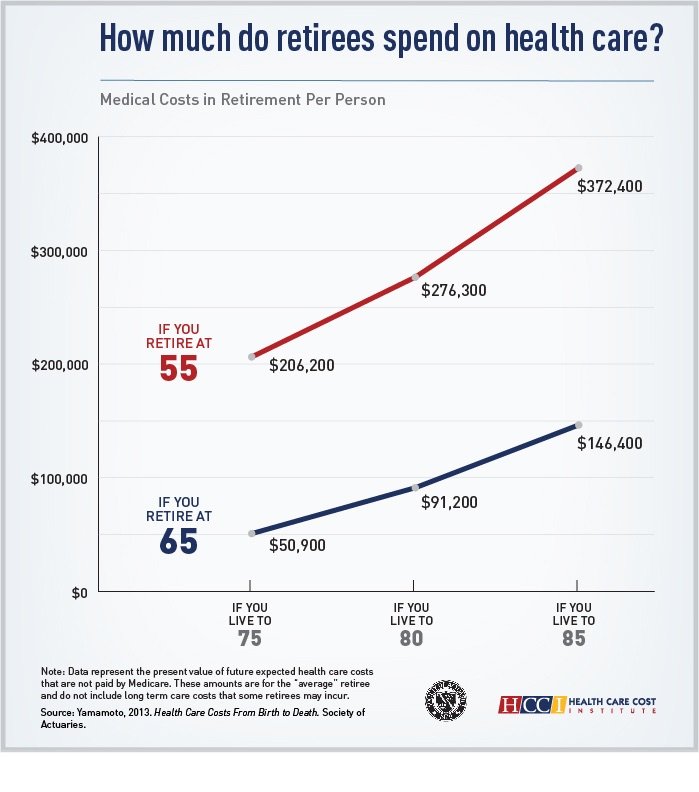

Meanwhile, life expectancy in the United States has risen by nearly 20 years since 1960, and a recent biotech boom in Silicon Valley hopes to continue that trend.

I think everyone can agree that this increase in life expectancy is wonderful – but it comes at a cost. For those who retire at age 55 and live to age 85, they can expect to pay $372,400 in medical costs per person. That’s nearly $750,000 for a married couple.

Healthcare costs are only part of the equation. The biggest expense for those age 55 and over is housing, accounting for 36-38% of total spending.

Baby boomers are facing a major income shortage during retirement. A recent BlackRock study found that boomers with a retirement fund hoped to generate $45k a year during retirement, but only saved enough to generate $10k per year. This lack of savings is consistent across all retirees, regardless of affluence or gender.

What does all this mean for American’s retiring seniors? They’re facing an income gap, over a longer period of time, and will be hit with increasing health care costs.

What’s a senior to do? Enter the reverse mortgage.

Reverse mortgages can be a safety net

Reverse mortgage loans are designed to fix these issues. Some seniors have large amounts of equity in their home, but do not have a substantial monthly income. When major expenses pop up and break their monthly budget, retirees have limited options –

- They could dip into their nest egg, which could further decrease their monthly income.

- They could take on debt, which is a short term solution and could potentially put their family in a tough situation upon their passing.

- They could leverage the equity in their home.

Prior to the creation of reverse mortgage loans, seniors had two options to access the equity in their home. They could refinance the home and take cash out – but that would create a new monthly payment and could affect monthly income. Or they could sell their home, which meant finding a new place to live.

To solve this issue Congress created the Home Equity Conversion Mortgages program in 1984, with loans insured by the Federal Housing Administration (FHA).

These Home Equity Conversion loans, often referred to as “reverse mortgages,” are for homeowners 62 years or older. It is a cash-out refinance loan, which means the borrower receives money, and in exchange, the lender uses equity in the home as collateral for the debt.

The thing that makes HECMs unique is they do not require the borrower to make a monthly payment to pay back the loan. Instead, the debt is repaid when the house is sold or homeowner passes.

This loan solves many issues for seniors –

- Ensures a stable housing situation and allows them to live in their family home.

- Lowers monthly payment amounts or eliminates the housing payment altogether.

- When cash is taken in a lump sum upfront, it can help cover large expenses like medical bills.

- When taken as a monthly draw, the cash can help cover living expenses.

In 1989, the first reverse mortgage loan was issued. Today thousands of reverse mortgages close every month, unlocking billions of dollars of home equity for cash-strapped seniors.

Reverse Mortgage Requirements

There are some basic criteria that must be met to qualify for an HECM loan, also known as a reverse mortgage. The most common question – “How old do you have to be to get a reverse mortgage?” As far as I know, these are the only loans that come with an age requirement – you have to wait to join the club!

Borrower requirements for a Reverse Mortgage

As a borrower, you need to be 62 years old to qualify for a reverse home loan. There are also a number of other requirements –

- Property must be owned outright, or have a significant amount of equity

- Property must be occupied as the primary residence (so no reverse mortgages on that vacation house!)

- Borrower must not be delinquent on any federal debt

- Borrow must have the ability to pay ongoing expenses outside of the mortgage payment. This includes property taxes, homeowners insurance, and HOA dues.

- Borrower must attend an information session with an approved HECM counselor.

Property requirements for a Reverse Mortgage

The property that will be mortgaged must also meet some simple qualifying criteria –

- Must be a single family home, or a 2-4 unit property with one unit occupied by the borrower

- If you lives in a condo, it must be a HUD-approved complex. If you’re not sure whether or not your condo qualifies, you look look it up here.

- If you live in a manufactured home, it must meet FHA requirements.

- The home must be properly maintained, and does not require a significant amount of work. If the property needs maintenance work or repairs, you can still close the loan – but the lender will require that part of the loan proceeds are used to complete repairs.

Once the mortgage is closed, the borrower is still required to make monthly payments that were not part of the mortgage debt payments. This includes property tax, homeowners insurance & HOA dues among other things.

Reverse Mortgages were made safer in 2016

In the past, reverse mortgages have had a bad reputation – partially due to predatory lenders, and partially due to some unforeseen circumstances.

The FHA & the Department of Housing and Urban Development (HUD) have continued to refine the program since it launched. Significant changes were made to make these loans safer for consumers – the most recent addition being a Financial Assessment for borrowers, which was launched in 2015.

To help you learn more about reverse home loans, we’ve put together some facts about reverse mortgages and a list of the reverse mortgage pros and cons you should consider.

HECM Financial Assessment

In the past, some borrowers with reverse mortgages have had difficulty making their property tax, insurance, or HOA payments. To fix that problem, and make reverse mortgages an even safer option for seniors, the FHA now requires lenders to perform a financial assessment of every borrower. We’ve included the financial assessment worksheet looks like, feel free to look it over in the viewer or download the PDF.

The financial assessment mostly affects the lender – it requires them to do much more research when qualifying the borrower, including:

- Performing a credit history analysis

- Analyzing cash flow & residual income

- Documenting and verifying credit, income, asset and property information

- Analyzing any external circumstances or extenuating circumstances

These are basic functions that most lenders would do for any mortgage. The big difference with the financial assessment for HECM loans is the lender calculates “set asides”. If the lender determines you may not be able to make certain payments (like property tax) they are required to take part of the loan proceeds and set money aside to help cover the payments.

How much money is set aside, if any, is affected by your monthly income. But it’s also affected by your age – due to the greater life expectancy, younger borrowers generally have to set aside more to ensure their expenses are covered.

{kind=link}